Diamond prices dropped in July, driven by slow retail sales and an oversupply in the Indian market. The seasonal summer slowdown also contributed to reduced sales figures.

Significant Price Reductions

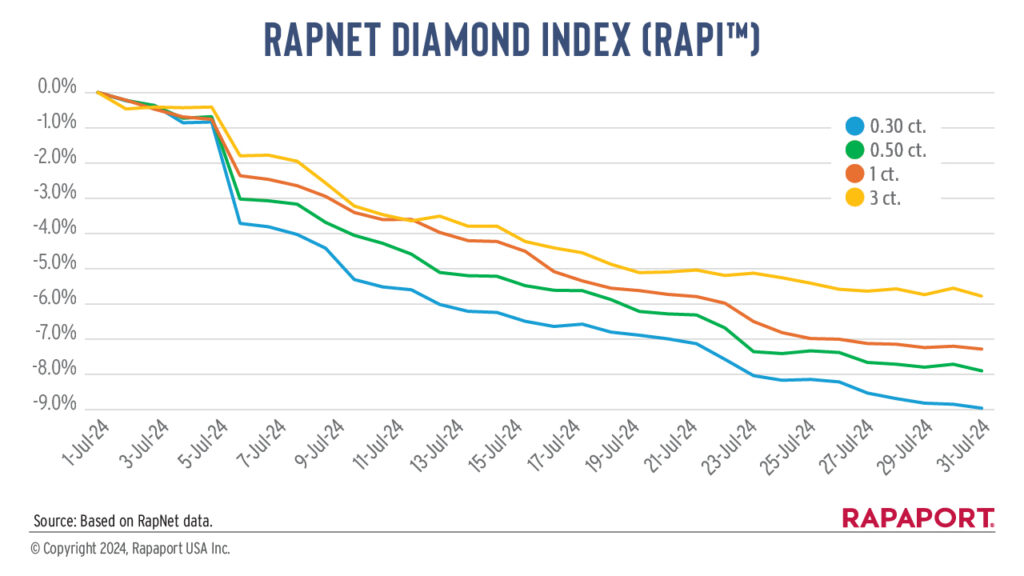

According to Rapaport’s RapNet Diamond Index (RAPI™), the index for 1-carat round, D to H, IF to VS2 diamonds fell by 7.3% in July, the steepest monthly decline for this size category since December 2008.

The RAPI for 0.30-carat diamonds dropped by 8.9%, while the index for 0.50-carat diamonds decreased by 7.9%. Prices for 3-carat stones saw a reduction of 5.8%. In contrast, 1-carat round, D to H, SI diamonds saw a more moderate decline of 3.2%, indicating steady demand from the US market.

Impact on Inventory and Production

The decrease in sales led to an increase in polished diamond inventory, with the number of diamonds listed on RapNet rising by 2% in July to reach a total of 1.7 million stones. From April 1 to August 1, this figure jumped by 9%.

To address the oversupply, Indian diamond manufacturers reduced production in July to align inventory with current demand levels. These production cuts are expected to impact inventory levels in about six weeks.

Sluggish Rough Diamond Demand

Rough diamond demand remained weak, with De Beers allowing sightholders to refuse goods at its July sight and offering 30% buybacks for certain categories. Sales for De Beers were estimated to be below $200 million.

Reduced Luxury Brand Purchases

Luxury brands have reduced their diamond purchases compared to previous years, causing weakness in the high-end diamond market. LVMH reported a 5% year-on-year decline in jewellery and watch sales, amounting to $5.58 billion in the first half of 2024. Additionally, LVMH highlighted slow US bridal demand, which has adversely affected Tiffany & Co.

Market Conditions in China and India

In China, diamond sales continued to be weak due to a sluggish economy and a shift in consumer behaviour away from diamonds as an investment. Consumers with higher spending power are choosing to spend on overseas travel rather than domestic purchases. In India, the jewellery industry anticipates strong domestic demand ahead of Diwali, reflected in the India International Jewellery Show (IIJS) running from August 8 to 13. Conversely, expectations for the September Jewellery & Gem World (JGW) Hong Kong show remain low amid continued weak demand in China.